Posted June 03, 2026

By Nick Riso

Someone Knows Something About Tesla

On Monday, someone spent $143,000 on Tesla Inc. (TSLA) options expiring this Friday.

People make directional bets on Tesla every day. So while $143,000 is real money, it's not an unusual size for an institutional options trade.

But then you look at the strike price.

The contracts give the buyer the right to purchase Tesla shares at $900. For reference, the stock is currently trading around $430.

Each contract costs, of course, next to nothing.

But for it to pay off, Tesla would have to double (and then some) before Friday's closing bell — just five trading days away from the trade.

That has never happened in Tesla’s entire history. Here’s the thing…

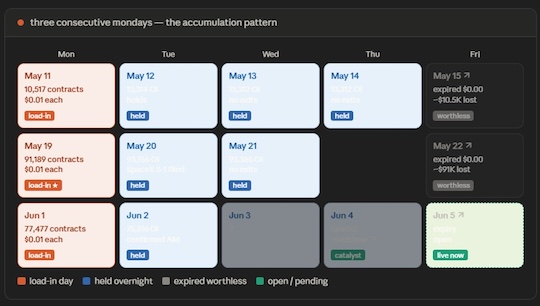

Whoever put on this trade did the exact same thing last Monday… and the Monday before that.

The contracts expired worthless both times. Tesla didn't double, the options went to zero, and hundreds of thousands of dollars evaporated.

Both times, they came back the following Monday with the same bet, the same strike, and a larger position.

There's a type of trade that only makes sense if you already know something.

The kind of knowing that arrives as a phone call, or a dinner, or an overheard conversation you were not supposed to overhear.

The kind no chart can tell you.

Total outlay across three weeks: hundreds of thousands of dollars. Total return: zero.

This is either the most patient gambler in the options market, or someone who’s not gambling at all.

Why This Is So Wild

To understand why this is strange, let’s talk about what a penny option actually is.

A $900 call on a $430 stock with five days to expiration is not really a financial instrument in any conventional sense.

The implied move required to make it pay is 117%. No single-week catalyst in the history of Tesla's publicly traded life has produced anything approaching that.

Not earnings beats, product launches, not even Elon Musk himself firing off acquisition tweets at 1 a.m.

The option's delta (its sensitivity to price movement) is so close to zero that it might as well live in a different zip code than the underlying stock.

It’s a near-mathematical impossibility dressed up as a trade. More precisely, it’s a bet on an announcement.

The person buying these contracts almost certainly does not believe Tesla will organically reach $900.

They believe that one day, possibly this Friday, someone with a microphone will say something that forces the market to reprice everything it thinks it knows about what Tesla is worth.

That person, most likely, is Elon Musk.

The Filing

On May 20, SpaceX filed its S-1 for what would be the largest initial public offering in the history of capital markets, a $1.75 trillion target valuation that would make the company worth more than every major automaker on earth combined.

The filing disclosed something that had not been widely understood — Tesla and SpaceX were already deeply financially entangled.

SpaceX had bought nearly $700 million in Tesla energy products. Tesla had invested $2 billion in SpaceX's absorbed AI subsidiary. The two companies were jointly building a semiconductor research facility at Gigafactory Texas. They shared engineers, supply chains, and a chief executive who had spent the better part of 2026 describing his companies as "trending toward convergence."

What Wall Street could not price was the simplest version of the question… what if Musk just said yes?

Said yes in the blunt transactional way he had said yes to Twitter and yes to xAI, which is to say yes to a number and a timeline that nobody expected and everyone had to immediately respond to.

If SpaceX's $1.75 trillion valuation folded into Tesla's existing market cap through a merger structured to keep Tesla as the surviving public entity, the math pointed to a per-share price somewhere above $900.

At penny-option prices, the cost of being right once easily absorbed the cost of being wrong twice.

The week of May 19 is the one that deserves the closest attention.

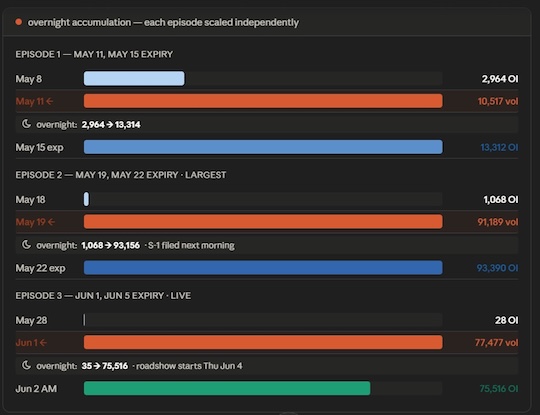

That Monday, 91,189 contracts crossed a single-day volume print that dwarfed everything that had come before it.

The next morning, SpaceX filed its S-1.

The position was sitting with 93,000 contracts of open interest when the document hit the SEC's servers, and it did not move.

Not a single contract closed.

The buyer did not take a profit on the news, did not trim the position, and did not react in any way that a speculator surprised by an unexpected development would react.

They just held and watched the contracts expire worthless three days later.

What does it mean to hold through news you bet on?

It means either the news was not the trigger and that there’s another specific event still outstanding. Or it means the buyer already knew the news was coming and understood, before markets opened, that the S-1 alone was not enough.

That the real trade required Musk to say the word.

Space Stocks… Circling the Moon Already?

While the anonymous buyer was quietly reloading, the rest of the market was doing something noisier and considerably more expensive.

In the weeks leading up to the SpaceX roadshow, retail options flow into space-adjacent names have been building steadily. Rocket Lab (RKLB), AST SpaceMobile (ASTS), Planet Labs (PL), the whole constellation of companies that trade on Musk-adjacent momentum.

The thesis was simple and wrong in the specific way that simple theses tend to be wrong in options markets. SpaceX goes public, space stocks go up, calls print.

What those buyers were not accounting for is one of the more reliable wealth-transfer mechanisms in derivatives trading.

It’s called volatility crush, which I covered a few weeks ago.

In the days before a known catalyst — an earnings report, a Fed decision, an IPO — options premiums inflate.

Market makers charge more for the uncertainty. Implied volatility, the number that sits inside every options price and functions as the market's estimate of future movement, rises in anticipation of the event.

Then the event happens. Implied volatility collapses, sometimes violently, taking option prices down with it — regardless of which direction the stock actually moved.

Someone who bought near-the-money RKLB calls in the week before the SpaceX roadshow could watch the underlying stock rally and still lose money, because the vol that was inflating their premium just got wrung out of the contract.

The $900 buyer has no such problem. At a penny, the contract carries almost no extrinsic value to crush.

Implied volatility has nowhere to fall because the option is already priced at the floor.

It is, among its other strange qualities, structurally immune to the very risk that will punish everyone else playing the same macro event.

The dumbest-looking trade in the options chain turns out to be better constructed than the smart money's roadshow plays.

The third Monday came on June 1.

The position rebuilt almost from scratch — 28 contracts of open interest going into that day, 75,516 by the following morning.

The SpaceX roadshow is scheduled to begin Thursday, June 4. Expiration: Friday, June 5.

The window between the roadshow opening and the Friday close is approximately 36 trading hours, the tightest the calendar has ever aligned around this particular bet.

Options markets are, among other things, a record of what people think they know.

Every contract represents a transaction between two parties who disagree about the future — one of whom is usually wrong.

But the $900 calls are something slightly different.

They are a pure unhedged bet that a binary event will occur before a specific date, not an expression of disagreement about Tesla's near-term fundamentals or a hedge against some correlated position or a piece of a complex spread.

The willingness to rebuild the position after two consecutive total losses, at an escalating size, is the behavior of someone who is waiting.

There is a word for trades like this in certain corners of the market.

The pattern — the specificity of the strike, the consistency of the weekly reset, the absence of any exit on news that should have moved the needle, the escalation — reads less like speculation and more like a reservation.

Someone has reserved a seat for an announcement they believe is coming.

They have now reserved it three times. Each week the seat goes unused, they buy a new ticket for the following Friday.

By Tuesday morning, the current ticket — 75,516 contracts, purchased the day before — was sitting in open interest, worth essentially nothing, waiting for Thursday…

Waiting for Elon.

Sign Up Today for Free!

Truth & Trends brings you market insights and trading tips you won't find anywhere else — unless you have your own personal hedge fund manager on speed dial...

Meet Enrique Abeyta, one of Wall Street’s most successful hedge fund managers. With years of experience managing billions of dollars and navigating the highs and lows of the financial markets, Enrique delivers unparalleled market insights straight to your inbox.

In Truth & Trends, Enrique shares his personal take on what’s moving the markets, revealing strategies that made him a star in the world of high finance. Whether it’s uncovering the next big trend or breaking down the hottest stocks and sectors, Enrique’s insights are sharp, actionable, and proven to work in any market condition.

Inside these daily updates, you’ll gain:

- 50 years of combined trading wisdom distilled into actionable insights.

- A behind-the-scenes look at how Wall Street pros spot opportunities and avoid pitfalls.

- Exclusive strategies that Enrique personally uses to deliver exceptional returns — no fluff, just results.

To have Truth & Trends sent directly to your inbox every weekday, just enter your email address below to join this exclusive community of informed traders.

Don’t miss your chance to learn from one of the best in the business.

Sign up now and take your trading game to the next level.

For Whom the IPO Bell Tolls (SpaceX)

Posted June 01, 2026

By Nick Riso

Reports of Software's Death Are Greatly Exaggerated

Posted May 29, 2026

By Greg Guenthner

SpaceX IPO: When EXACTLY to Buy

Posted May 28, 2026

By Enrique Abeyta

Everyone Knows the Market Is Rigged. But How?

Posted May 22, 2026

By Greg Guenthner

The Death of Laissez-Faire Capitalism

Posted May 21, 2026

By Enrique Abeyta