Posted May 20, 2026

By Nick Riso

Welcome to the Dark Side of the Moon

Nobody told the guy in the elevator he was holding a melting ice cube.

He'd bought the calls — an options bet that a stock would go up — three days before earnings. He felt smart about it, watched the stock gap up 4% the next morning, and checked his account to find his position down 15%.

The stock had moved in exactly the right direction. The bet was fundamentally correct…

And the money was gone anyway.

Welcome to IV crush, the options market's most elegant tax on the impatient and the uninitiated.

The space sector is about to become a master class in this particular phenomenon.

SpaceX's IPO — now confirmed, targeting a June 12 Nasdaq debut under the ticker SPCX at a valuation somewhere between $1.75 and $2 trillion — will be the most anticipated equity event in a generation.

A wave of retail traders is going to buy calls on every publicly traded space stock the day the S-1 drops, sit back feeling prescient, and discover that the market had already priced in their optimism weeks before they arrived.

Some of them will lose money on trades that were fundamentally correct. Where the thesis played out, the stock moved, and the math betrayed them anyway.

This piece is for those people, written before the fact.

The Physics of Expensive Air

Options are priced on two things.

The first is intrinsic value, how much a contract is already "in the money," meaning how far the strike price is from where the stock actually trades.

The second, and the one that kills people, is extrinsic value: the time premium, the market's live estimate of how much things might change before expiration.

That estimate gets expressed as a single number called implied volatility, or IV, and it behaves like atmospheric pressure — you can't see it directly, but you feel it in everything around you.

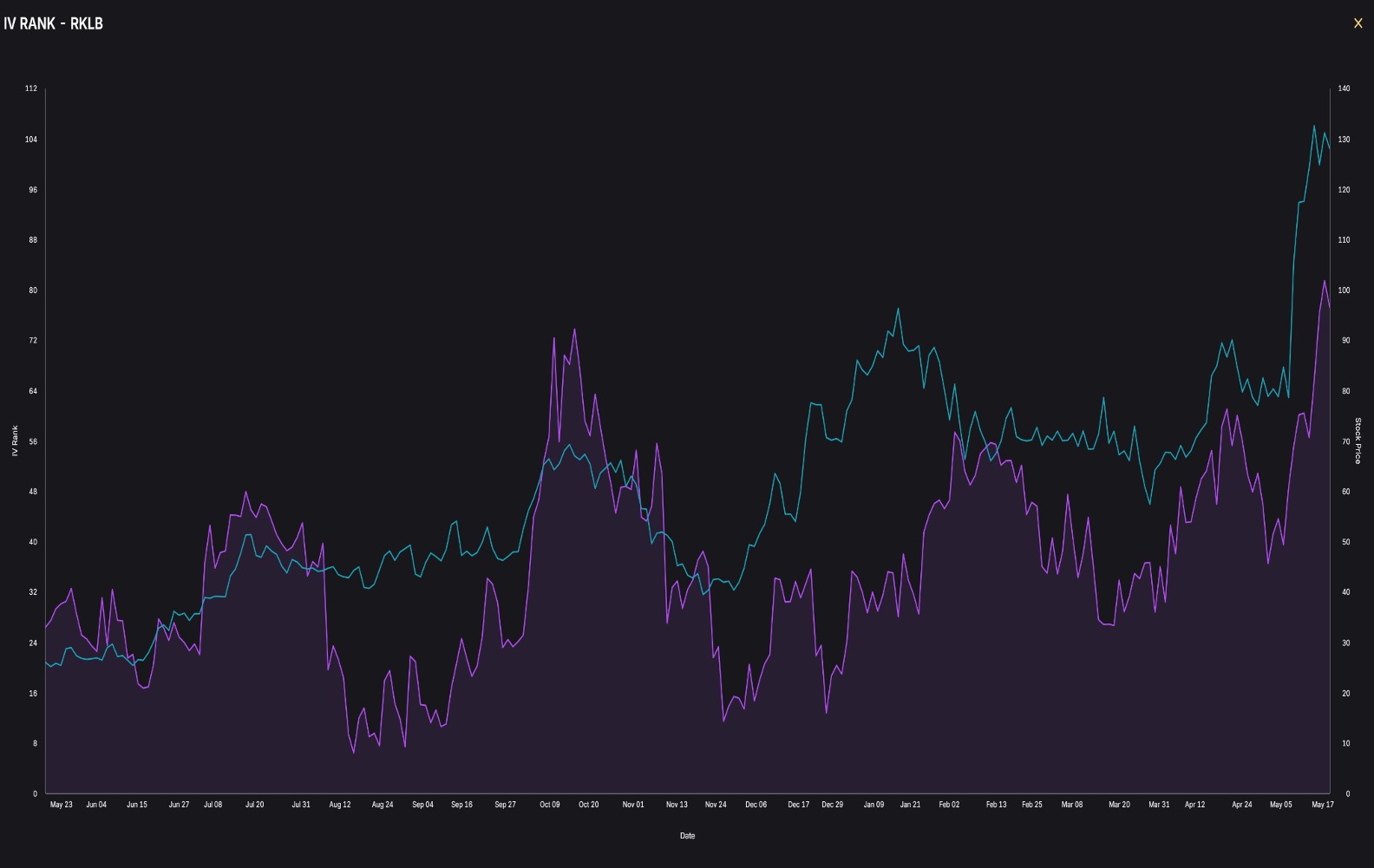

Pull up Rocket Lab (RKLB) right now, which has gone from a $24 stock to $128 in the past 12 months.

You’ll find a company whose options market is pricing in a 30-day implied move of roughly $26 against that $128 stock price, a 20% expected swing in a single month, with an IV rank of 77.

That means the market is currently more uncertain about Rocket Lab than it has been on more than three out of every four trading days in the past year.

AST SpaceMobile (ASTS), the satellite-to-cell-phone company that has quietly become one of the most interesting stories in the sector, sits at an IV rank of 82 with a 30-day implied move of more than $20 against a stock in the mid-$80s.

Intuitive Machines (LUNR) clocks in at 74, and Redwire (RDW) is pinned at a 99 IV rank today, meaning its options are more expensive than they have been on essentially every single trading day in the past year.

What all of these numbers are telling you, collectively, is that the market is charging a lot of money for the right to be right — and that premium has to come from somewhere. It comes from you.

The Quiet Extraction Mechanism

Here is how IV crush works in practice.

Say a company has earnings in two weeks, and the market doesn't know whether it's going to beat or miss. That uncertainty is real and quantifiable, and the options market prices it in by expanding implied volatility, pushing up the cost of every contract that spans the event.

You buy a call for $5, the company reports a blowout quarter, the stock jumps 3%, and when you check your position, you find the contract sitting at $4.10, which makes no sense until you understand that what you were paying for wasn't the direction of the move but the uncertainty surrounding it.

The moment earnings resolved and that uncertainty evaporated, IV collapsed — rapidly, violently — and dragged the extrinsic value of your contract down with it.

This is where vega enters the picture, and it matters enormously in space stocks specifically because these names carry such elevated IV to begin with.

Think of vega as your option's sensitivity to the market's fear gauge — specifically, it measures how much an option's price changes for every one percentage point move in implied volatility.

A contract with a vega of 0.25 loses 25 cents for every point IV drops and gains 25 cents for every point it rises, and in a high-IV environment like the one space stocks are living in right now, that number drives more of your P&L than the stock's actual direction.

When SpaceX files its S-1 and every space stock gets a sympathy rally — and they will, because RKLB and ASTS and LUNR will all be treated as either direct competitors, halo beneficiaries, or both — IV across the sector is going to surge, and the vega embedded in your contracts will print beautifully on the way up.

The problem is what happens on the other side — the moment the IPO prices, or the lockup provisions become clear, or the first post-IPO earnings call lands, IV will collapse with the same speed it inflated, and vega, which was your friend, becomes the mechanism of your destruction.

The Ramp You're Already Late To

The thing that makes this trade so instructive is that you can watch it happen in real time, in the data, like a slow-motion replay of a play you missed.

On March 25, Reuters first reported that SpaceX was eyeing a mid-2026 IPO.

RKLB jumped 11% that day.

That was the starting gun, and the options market heard it clearly.

RKLB's IV rank on April 9 — two weeks after the initial report — sat at roughly 43, meaning the market was still digesting the news, still pricing the uncertainty at a relatively modest level.

You can see that in the purple line above.

The traders who were paying attention bought their vega there, while it was still on sale.

Watch what happened next.

By late April, RKLB's IV rank had climbed into the low 50s.

By early May, the S-1 timeline sharpened — Reuters reported a prospectus as early as today, a roadshow kicking off June 4, pricing June 11, listing June 12 — and the IV rank climbed again, touching the mid-60s on May 14 as SpaceX disclosed a 5-for-1 stock split and speculation became something closer to certainty.

By May 18, it sat at 81.

Today it's at 77, and the implied 30-day move on RKLB is $26 — nearly a quarter of the stock's price, priced into your option before you've done a single thing.

That is the IV ramp. You didn't miss the rocket! You missed the rumor.

The Tape Already Knows Things

The institutional money tends to understand all of this better than anyone, which is part of why watching where the real size goes tells you so much.

In the past two weeks alone, the flow on RKLB and ASTS has been illuminating.

On RKLB, a cross trade printed on May 15 — 1,300 contracts in the March 2027 $155 calls at $31.39 apiece, roughly $4 million in premium, and on the same day via the same mechanism, 1,300 contracts in the March 2027 $110 puts at $29.37.

That is a structured, long-dated position spanning multiple potential catalysts, with both legs sitting too far from the money to be simple directional bets, and it reads like someone positioning for a wide range of outcomes across a horizon that includes not just the next earnings cycle but whatever happens in the competitive landscape when SpaceX is finally public.

They are not buying a one-month call and hoping for a pop. They are paying for time and for vega and doing it before the narrative fully inflates.

On ASTS, the standout print was a $7.8 million cross trade in the July $80 puts — 5,600 contracts executed on May 14 with ASTS trading around $80, carrying an IV reading around 106%.

Whether that's institutional hedging against a long equity position or an outright directional bet, whoever put that on was paying $13.95 per contract when ASTS IV was already elevated, which means they weren't buying into quiet — they were buying into noise, with enough size and structure to suggest they know exactly what they own.

The reason sophisticated money is positioning in these names right now, even with the IPO just weeks away, is that they're playing a different game than the people who will buy calls on listing day.

They are not betting on SpaceX.

They are betting on the anticipation of SpaceX, and those are two very different trades with very different risk profiles.

The Strategy Nobody Talks About

The counterintuitive play — the one that works in event-driven situations across every sector, not just space — is to buy IV before it runs and sell before the event resolves.

This cuts against the instinct of most retail traders who wait for conviction, who want to feel certain before committing, who end up buying right before the thing happens precisely because that's when the story feels most obvious, and the trade feels most justified.

But that moment of maximum narrative clarity is also the moment of maximum IV, when the market has already charged you the full uncertainty premium, and the only direction volatility can realistically travel once the event resolves is down.

The people who make money in event-driven options are usually the ones who correctly called when the anticipation would peak.

In practice, this means identifying the catalyst, buying options in the quiet before the crowd arrives, and then selling into the hype — ideally five to ten days before the event itself — at which point your contracts are priced with elevated IV baked in, and you exit not because the event went wrong but because you've already monetized the uncertainty expansion.

Whatever happens next, whether the rocket succeeds or the IPO pops or the earnings beat, is no longer your problem.

The IV crush that follows belongs to whoever bought your contracts.

The RKLB $130 calls expiring June 18 offer a useful illustration, with six consecutive days of open interest increases on that contract and IV sitting above 100%.

Anyone who bought those calls when IV rank was in the low 40s back in early April is sitting on a position that appreciated not just because RKLB went from $70 to $128, but because the cost of uncertainty itself more than doubled.

Held into the IPO listing day, those same contracts are now exposed to a violent reversal in the other direction.

Sold five days before the Nasdaq debut, the story ends very differently.

None of this is risk-free, and it shouldn't be presented as such, because IV doesn't always run on the schedule you expect, stocks move for reasons that overwhelm volatility calculations, and timing the peak of anticipation is genuinely difficult.

Being too early means watching your contracts decay while you wait for the crowd to show up.

But the core principle holds: you make money in event-driven options by selling uncertainty, not by holding through its resolution.

What the Architecture of a Smart Trade Looks Like

Given all of this, a coherent framework for trading space stocks into the SpaceX IPO involves identifying the catalysts that create IV expansion…

The S-1 filing, the roadshow, the pricing, the first day of trading, the inevitable competitor announcements that follow…

And building positions in the quiet before the crowd assigns maximum narrative value to the names, using structures that favor vega exposure through longer-dated options that don't bleed time value as aggressively, and perhaps spreads that cap both upside and downside to reduce the raw premium you're paying into an already-elevated IV environment.

Then sell into the frenzy, not after it, because the day everyone is talking about space stocks is the day you want to be closing positions rather than opening them.

The news flow that feels like a tailwind is, from the options market's perspective, simply a signal that uncertainty is about to be resolved — and resolution is the enemy of extrinsic value.

The only people guaranteed to make money when SpaceX goes public are the people who already own SpaceX.

For everyone else, the question is whether you're buying the rocket or buying the rumor, and while the rocket gets all the attention, the rumor is where the money is.

Sign Up Today for Free!

Truth & Trends brings you market insights and trading tips you won't find anywhere else — unless you have your own personal hedge fund manager on speed dial...

Meet Enrique Abeyta, one of Wall Street’s most successful hedge fund managers. With years of experience managing billions of dollars and navigating the highs and lows of the financial markets, Enrique delivers unparalleled market insights straight to your inbox.

In Truth & Trends, Enrique shares his personal take on what’s moving the markets, revealing strategies that made him a star in the world of high finance. Whether it’s uncovering the next big trend or breaking down the hottest stocks and sectors, Enrique’s insights are sharp, actionable, and proven to work in any market condition.

Inside these daily updates, you’ll gain:

- 50 years of combined trading wisdom distilled into actionable insights.

- A behind-the-scenes look at how Wall Street pros spot opportunities and avoid pitfalls.

- Exclusive strategies that Enrique personally uses to deliver exceptional returns — no fluff, just results.

To have Truth & Trends sent directly to your inbox every weekday, just enter your email address below to join this exclusive community of informed traders.

Don’t miss your chance to learn from one of the best in the business.

Sign up now and take your trading game to the next level.

Trump Meets Xi for “Crisis Summit” 2026

Posted May 18, 2026

By Enrique Abeyta

3 Tickers to Watch as the Semi Trade Unwinds

Posted May 15, 2026

By Greg Guenthner

The $16 Trillion China Summit

Posted May 14, 2026

By Enrique Abeyta

The Tell-Tape Heart

Posted May 13, 2026

By Nick Riso

All-Time Highs... in THIS Economy?

Posted May 11, 2026

By Enrique Abeyta