Posted May 13, 2026

By Nick Riso

The Tell-Tape Heart

There’s a version of events in which Micron's stock price over the last three weeks reflects something real.

Analysts have been upgrading their targets. There's institutional conviction in the AI memory cycle. And the market is efficiently pricing a company whose chips sit at the center of the most consequential infrastructure buildout in a generation.

Everyone keeps saying that semiconductors are the oil of the 21st century, and Micron makes the refineries.

Last Friday, the stock was up 15% on the day, capping its best week in two decades. Currently, it's trading near all-time highs above $800.

MarketWatch noted that it was now worth more than JPMorgan, and CNBC called the rally parabolic.

The brokerage notes were falling over each other.

That version is clean and legible… and almost certainly wrong.

The actual mechanism driving Micron's price is sitting in the options tape. It has everything to do with arithmetic — and almost nothing to do with conviction.

Let’s Look Under the Hood

When you buy a call option on a stock, someone has to sell it to you.

That someone is almost always a market maker, a dealer whose entire business model depends on staying directionally neutral — on never actually caring whether the stock goes up or down.

To stay neutral after selling you a call, the dealer has to buy the underlying stock. Not because they want to, of course. But because their risk model requires it.

The amount they buy is determined by the option's delta, a measure of how much the option's value moves relative to the stock.

A call with a delta of 0.30 means the dealer buys 30 shares for every 100-share contract. As the stock rises and the call moves closer to being in the money, the delta increases and the dealer buys more shares.

As the stock rises further, they buy more still. They’re doing math, not making bets.

This is the mechanism. And it’s why the options market matters in Micron's case specifically.

When you have hundreds of thousands of people buying calls on the same stock in the same week, the dealers who sold those calls are collectively purchasing enormous quantities of the underlying shares.

It’s as simple as this…

The stock goes up. The calls get more valuable. More people buy calls. The dealers buy more stock. The stock goes up again. The people who bought calls last Monday feel vindicated and buy more this Monday. Around and around and around we go.

What makes this unstable is what happens when it stops.

The calls expire Friday afternoon. The dealers who were long Micron stock to hedge those calls no longer need to be, so they unwind.

If the crowd comes back Monday and reloads — and for 15 straight sessions they have — the hedge book rebuilds and the stock finds its footing.

But if they come back smaller, or if something spooks them, or if the expiration Friday is large enough that the unwind overwhelms the new buying, the stock loses the only thing that was actually holding it up.

There is no fundamental buyer waiting underneath. There is just the absence of a mechanical one.

Into the Numbers

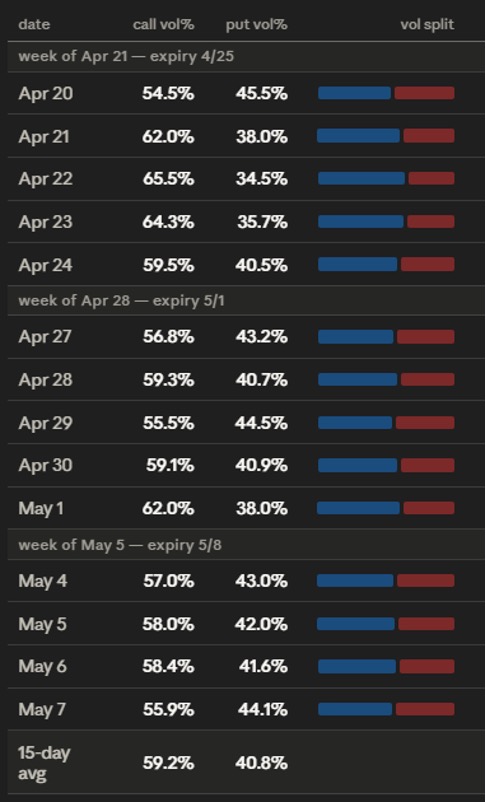

For 15 consecutive trading sessions (April 20–May 8), roughly half of all options volume on Micron expired that same Friday.

The number was 48% on April 20, a Monday. It was 51.9% on April 22, a Wednesday. On May 7, a Thursday, one day before expiration, it reached 57.3% — the highest reading in the entire dataset.

The crowd was accelerating exposure into expiration.

On May 8, 1.6 million contracts changed hands, the largest single session in the period. And 848,000 of them (53.1%) expired that afternoon.

Over the course of my analysis, this three-week period, the number never dropped below 47%.

Calls dominated volume every single day, averaging 59.2% of all contracts traded. Some days the skew was more dramatic — 65.5% on April 22, 62% on both April 21 and May 1.

There was not a single session in which puts led volume. To look at the tape, Micron was the most straightforwardly bullish major semiconductor in the market.

Everyone was buying upside. But there’s a wrinkle in this story.

We have to understand first and foremost that volume is what people do today.

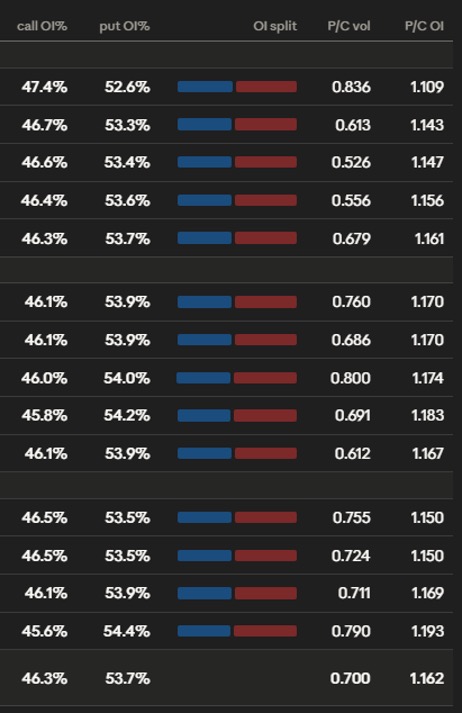

Open interest is what they're still holding when the market closes. And open interest told a completely different story.

Puts outnumbered calls in open interest every single day.

The put-to-call ratio in open interest started the period at 1.109 on April 20 and ended it at 1.193 on May 7, grinding higher session by session without a single reversal.

On the days when call volume was most lopsided — when the tape looked most bullish — the put book underneath kept getting heavier. Every Friday, the weekly calls burned off. And every Monday, the puts were still there.

Not once did the two stories converge.

What this means is that two completely different groups of people have been participating in Micron's options market simultaneously. And they have been making opposite bets.

Two Camps

The first group is loud. You know who I mean…

They buy calls that expire Friday, generate the volume that moves across the tape, and create the dealer hedging flows that push the stock higher. Their wins are fast and visible. Their losses are total and weekly, and they come back anyway.

The second group is quiet. They don't show up in the volume numbers — they show up in the open interest, accumulated position by position over weeks, and they are overwhelmingly on the other side.

The question worth asking is which group has been paying more attention to the actual structure of what's happening.

Implied volatility (the market's expectation of future price movement baked into options prices) has been rising for three weeks alongside the stock.

This is the kind of thing that gets dismissed as a technical footnote but is actually one of the more reliable warning signs available.

When a bull market is healthy, volatility compresses as prices rise.

The move confirms the thesis. Uncertainty resolves and options get cheaper.

In Micron's market, the opposite has happened.

Volume-weighted average IV was 79.8% on April 20. By May 7, it was 100.5%, and it had been above 100% for multiple sessions. The market was pricing in bigger and bigger potential moves even as the crowd bought calls expecting the stock to grind higher in an orderly way.

These two things cannot both be right at the same time.

More telling than the level is the shape.

On April 20, near-term implied volatility (on contracts expiring within two weeks) was 79.6%. Far-term IV was 79.9%. The curve was flat, which is normal. By May 7, near-term IV was 105.4% and far-term IV was 84.4%.

The curve had inverted.

The market was pricing in more uncertainty for the next two weeks than for the next six months. This is a condition that resolves, and it resolves through price.

Then there is what happened on May 8, expiration Friday, the biggest session in the dataset.

The largest block trades that day were not calls.

They were puts — deep out-of-the-money puts, struck at $405, bought on the ask at implied volatilities between 164% and 171%. The largest single print was 8,442 contracts. Then 6,000 more at the same strike… Then 4,000 more.

Over 18,000 contracts in a cluster, all pointing the same direction, all paying extraordinary premiums for the right to profit from a move that would require Micron to fall sharply from where it was trading.

The delta on these contracts was essentially zero, and they weren’t hedges. A hedge is sized efficiently against a known risk. These were a bet, placed by someone who looked at the most bullish-looking tape in the semiconductor space and decided the risk worth paying for was catastrophic downside.

The last piece is the one that is hardest to dismiss.

Far-dated options — contracts expiring more than two weeks out, insulated from the weekly gamma noise, priced by people making longer-horizon decisions — averaged $1,732 per contract on April 20.

By May 7, the average had reached $8,848. A 5.1x increase in 15 trading days.

Far-dated options don't get that expensive because of retail momentum. They get that expensive because someone with a longer time horizon is making a considered decision to pay significantly more for exposure that won't resolve this Friday or next.

The near-term crowd got louder while the long-term crowd got more expensive.

They are not describing the same market.

Gamma squeezes are not unusual. Stocks get caught in them, run hard, and eventually the structure exhausts itself.

What is unusual about Micron is the duration, the consistency, and the scale of the divergence between what the volume says and what the open interest says — between what the crowd is doing and what the patient money underneath has been building for three weeks.

Micron is silver in 2025 leading up to the late January reckoning. Where precisely it is, we don’t exactly know. What we do know is that this doesn’t end well.

The crowd has been right about the direction. The question is whether they understand what has been generating it and what happens when it stops.

The calls expire on Friday. They always do.

The puts are still there on Monday morning. They always are.

At some point, those two facts are going to matter at the same time.

Sign Up Today for Free!

Truth & Trends brings you market insights and trading tips you won't find anywhere else — unless you have your own personal hedge fund manager on speed dial...

Meet Enrique Abeyta, one of Wall Street’s most successful hedge fund managers. With years of experience managing billions of dollars and navigating the highs and lows of the financial markets, Enrique delivers unparalleled market insights straight to your inbox.

In Truth & Trends, Enrique shares his personal take on what’s moving the markets, revealing strategies that made him a star in the world of high finance. Whether it’s uncovering the next big trend or breaking down the hottest stocks and sectors, Enrique’s insights are sharp, actionable, and proven to work in any market condition.

Inside these daily updates, you’ll gain:

- 50 years of combined trading wisdom distilled into actionable insights.

- A behind-the-scenes look at how Wall Street pros spot opportunities and avoid pitfalls.

- Exclusive strategies that Enrique personally uses to deliver exceptional returns — no fluff, just results.

To have Truth & Trends sent directly to your inbox every weekday, just enter your email address below to join this exclusive community of informed traders.

Don’t miss your chance to learn from one of the best in the business.

Sign up now and take your trading game to the next level.

All-Time Highs... in THIS Economy?

Posted May 11, 2026

By Enrique Abeyta

The "Killer Bees" Are Swarming Again

Posted May 08, 2026

By Greg Guenthner

The MU-mentum Trap: When Good Trades Go Bad

Posted May 07, 2026

By Enrique Abeyta

Coming Soon: The YOLO Market, Unleashed

Posted May 01, 2026

By Greg Guenthner

The First Berkshire Meeting After Buffett - Now What?

Posted April 30, 2026

By Enrique Abeyta