Posted July 16, 2026

By Enrique Abeyta

The One Question I Ask Before Buying Any Stock

Every earnings season, I find myself doing the same thing.

I stop worrying about individual stocks, analyst price targets, or whether the Fed is about to cut interest rates.

Instead, I step back and ask myself one simple question…

What kind of market am I investing in?

It may sound simplistic. But after decades of investing, I've come to believe that answering this question correctly is one of the most important things an investor can do.

The reason is straightforward.

You can identify a wonderful business, buy it at a reasonable price, and still lose money if you've misjudged the broader market.

But when you've correctly identified the market's primary trend, investing is dramatically easier because you're working with the tide instead of swimming against it.

That's why, before I decide whether a stock is worth buying, I first determine whether the environment favors owning stocks.

Bull markets tend to be forgiving.

Strong companies usually outperform, good companies are rewarded for solid execution, and even mediocre businesses can rise simply because capital is flowing into equities.

Bear markets are different.

I've traded through several of them successfully, so I'm certainly not suggesting money can't be made.

But anyone who's lived through a bear market knows the environment changes dramatically.

Investors become defensive. Valuations compress. Good earnings often get ignored. Fear replaces optimism, and every investment decision becomes more difficult.

That's why I always start by identifying the market.

Only then do I decide how aggressive I want to be.

Now that we’re at the halfway point of 2026 and going into another earnings season, I think it's worth asking the question again.

Are we still in a bull market?

Everyone Is Asking the Wrong Question

I recently read an excellent article by Ryan Detrick and the team at Carson Group titled More Reasons to Be Bullish the Rest of 2026.

Their historical research made a compelling case that this bull market may still have room to run. And I agreed with many of their conclusions.

More importantly, the article reinforced something I've believed for a long time.

I think most investors are asking the wrong question.

Every time the market reaches a new high, the conversation immediately shifts to valuation.

"Aren't stocks too expensive?"

It's a fair question. I just don't think it's the most important one.

Instead of asking whether stocks are expensive, I think investors should be asking why they're expensive.

History is filled with companies that looked outrageously expensive before becoming some of the greatest investments of their generation. Amazon. Apple. Microsoft. Nvidia.

But those companies didn't become expensive because investors suddenly became irrational. They got there because their earnings power changed.

And bull markets usually keep going until the reasons investors are willing to pay those higher prices begin to disappear.

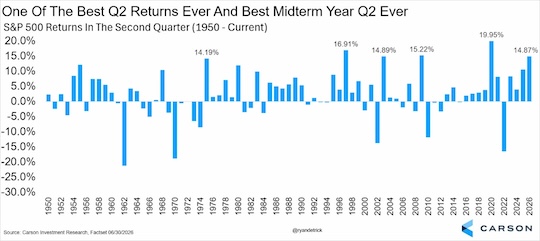

That brings me back to Ryan Detrick's research. One chart in particular immediately caught my attention.

Source: Ryan Detrick of Carson Group

Source: Ryan Detrick of Carson Group

Despite tariffs, geopolitical uncertainty, inflation concerns, and constant warnings of an AI bubble, the S&P 500 just completed one of its strongest second quarters since 1950.

Think about that for a moment.

Bull markets can keep going even during imperfect conditions. They just need reality to turn out better than investors expected.

This week's Consumer Price Index offered another good example.

Inflation continued moving in the right direction.

No, one report doesn't guarantee anything.

But taken together with resilient corporate earnings and a durable economy, the evidence still suggests an environment that supports higher stock prices.

Rotation Isn't the Same as Retreat

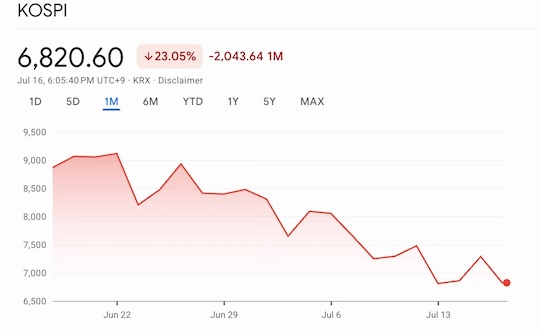

The market recently handed us a perfect case study.

Memory stocks, among the hottest investments on the planet just a few weeks ago, came under heavy selling pressure.

Semiconductor stocks followed suit, and South Korea's KOSPI Index, which had become one of the world's strongest equity markets, slipped into correction territory.

Source: Google Finance

Source: Google Finance

If you only followed the headlines, you could easily conclude that the AI trade was beginning to unravel.

I don't think that's what happened.

In fact, I think the market was doing exactly what healthy bull markets often do: It was rotating.

Over the past several months, I've talked a lot about AI, semiconductor demand, and memory chips.

None of those long-term drivers suddenly disappeared. What changed was investor positioning.

Some of the market's most popular trades had become crowded. Expectations were elevated, momentum had become stretched, and investors began locking in profits.

That's not unusual. In many ways, it's healthy.

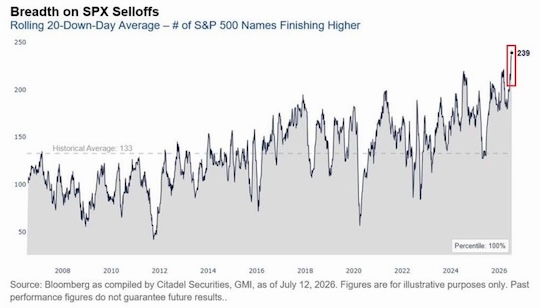

One statistic I came across this week reinforced something I've observed throughout my investing career.

Source: Citadel Securities

Source: Citadel Securities

During the last 20 trading sessions in which the S&P 500 finished lower, an average of 239 companies in the index finished higher.

Think about what that means.

The headlines told us the market was falling. But the market itself told us money was simply moving elsewhere.

Healthy bull markets don't require every sector to rise together. Leadership rotates, and one group cools off while another takes the baton.

That's fundamentally different from investors abandoning equities altogether.

Understanding that difference can keep investors from making some very expensive mistakes.

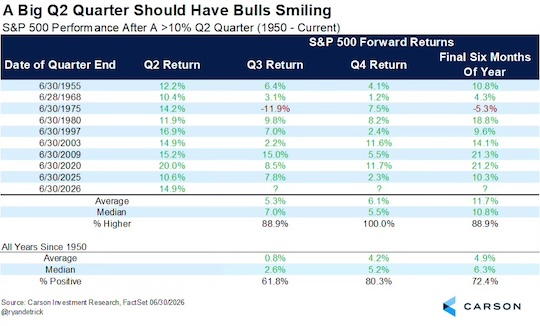

Ryan Detrick's second chart reinforces that idea.

Source: Ryan Detrick of Carson Group

Source: Ryan Detrick of Carson Group

Historically, markets that produce exceptionally strong first halves have often gone on to deliver respectable second halves as well.

Notice I said often. Not always.

The point is that healthy bull markets generally remain healthy until something meaningful changes.

So, what would make me change my mind?

3 Things That Historically End Bull Markets

We all know that every bull market eventually ends. The challenge is recognizing why.

For me, there are three developments that deserve far more attention than the daily headlines.

The first is a meaningful deterioration in corporate earnings.

Again, bull markets don't usually die because stocks become expensive. They end because earnings stop justifying those valuations.

As we move through another earnings season, that's where my attention will be focused.

The second is a weakening economy that points toward recession.

So far, we've experienced something many economists believed was impossible: inflation has cooled while the economy has remained remarkably resilient.

If that relationship changes, my outlook will change with it.

And finally, I'll be watching for restrictive monetary policy.

If you study the major bear markets of recent history, this appears with surprising frequency.

The bursting of the dot-com bubble followed a tightening cycle.

The financial crisis unfolded after years of rising rates.

More recently, the 2022 bear market was driven largely by one of the fastest rate-hiking campaigns in modern history.

That's one reason this week's CPI report mattered. Cooling inflation reduces the likelihood that policymakers will need to tighten policy again.

The Truth

Every earnings season, Wall Street gives investors a new reason to panic. This time around, it was semiconductor stocks, memory stocks, and the latest fears surrounding AI.

However, the market told a much more nuanced story.

Inflation continues cooling…

Corporate earnings remain resilient…

Market participation is broadening…

And capital appears to be rotating rather than leaving equities.

Could that change? Absolutely.

And eventually, it will. Bull markets don't last forever.

But they also don't end because a handful of popular stocks correct 15%.

They end because the environment that supported them fundamentally changes.

That's the change I'll continue watching for.

Until then, I'll keep asking myself the same question I've asked before every major investment decision throughout my career.

What kind of market am I investing in?

After weighing the evidence — not the headlines — my answer hasn't changed.

I'll tune out the noise, focus on the fundamentals, and let the market tell me when the trend has truly shifted.

So far, it hasn't. And until the evidence tells me otherwise... I'm staying invested.

Sign Up Today for Free!

Truth & Trends brings you market insights and trading tips you won't find anywhere else — unless you have your own personal hedge fund manager on speed dial...

Meet Enrique Abeyta, one of Wall Street’s most successful hedge fund managers. With years of experience managing billions of dollars and navigating the highs and lows of the financial markets, Enrique delivers unparalleled market insights straight to your inbox.

In Truth & Trends, Enrique shares his personal take on what’s moving the markets, revealing strategies that made him a star in the world of high finance. Whether it’s uncovering the next big trend or breaking down the hottest stocks and sectors, Enrique’s insights are sharp, actionable, and proven to work in any market condition.

Inside these daily updates, you’ll gain:

- 50 years of combined trading wisdom distilled into actionable insights.

- A behind-the-scenes look at how Wall Street pros spot opportunities and avoid pitfalls.

- Exclusive strategies that Enrique personally uses to deliver exceptional returns — no fluff, just results.

To have Truth & Trends sent directly to your inbox every weekday, just enter your email address below to join this exclusive community of informed traders.

Don’t miss your chance to learn from one of the best in the business.

Sign up now and take your trading game to the next level.

The Biggest IPO You Never Heard About

Posted July 13, 2026

By Enrique Abeyta

My Tesla Calls Went to Zero... Just as I Planned

Posted July 10, 2026

By Greg Guenthner

Mark Twain Was Right About Your Newsfeed

Posted July 09, 2026

By Enrique Abeyta

Six Months In: My 2026 Report Card

Posted July 06, 2026

By Enrique Abeyta

The S-E-T System for Finding Breakout Stocks

Posted July 03, 2026

By Greg Guenthner